What is TDS?

Definition of TDS

Tax Deducted at Source (TDS) is a mechanism introduced by the Indian government to collect tax at the source of income. Under this system, a certain percentage of the payment is deducted by the payer before making the payment to the recipient. The deducted amount is then deposited with the government.

Purpose of TDS

The primary purpose of TDS is to ensure tax compliance and prevent tax evasion. By deducting tax at the source, the government can collect revenue more efficiently.

TDS on Foreign Remittances

Overview of Foreign Remittances

Foreign remittances refer to the transfer of money from residents of India to non-residents or foreign entities. These transactions are common in various contexts, including:

- Payments for services rendered

- Royalties

- Technical fees

- Interest payments

- Dividend payments

TDS Applicability

TDS applies to foreign remittances when the payments are made to non-residents for services rendered or income received in India. The applicability of TDS depends on the nature of the payment and the provisions of the Income Tax Act.

TDS Rates for Foreign Remittances

TDS rates on foreign remittances vary based on the type of payment and the provisions laid out in the Income Tax Act. Below are some of the common payments and their applicable TDS rates:

1. Payments for Technical Services

- Rate: 40% (plus applicable cess)

- Section: 194J

- Details: This applies to payments made for technical services provided by foreign entities.

2. Payments for Professional Services

- Rate: 40% (plus applicable cess)

- Section: 194J

- Details: Similar to technical services, this rate applies to professional services rendered by non-residents.

3. Payments for Royalties

- Rate: 40% (plus applicable cess)

- Section: 194J

- Details: Royalties paid to foreign entities are subject to TDS at this rate.

4. Interest Payments

- Rate: 40% (plus applicable cess)

- Section: 194A

- Details: Interest payments made to non-residents are also subject to TDS at this rate.

5. Payments for Sale of Goods

- Rate: 40% (plus applicable cess)

- Section: 195

- Details: Payments for the sale of goods to foreign entities fall under this section.

6. Dividend Payments

- Rate: 40% (plus applicable cess)

- Section: 194

- Details: Dividends paid to foreign shareholders are subject to TDS.

7. Other Payments

- Rate: 40% (plus applicable cess)

- Details: Payments for any other services not explicitly mentioned may also be subject to TDS at the rate of 40%.

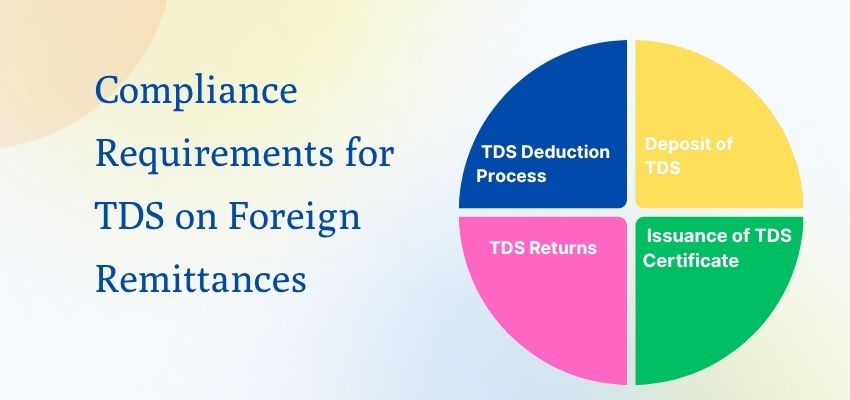

Compliance Requirements for TDS on Foreign Remittances

1. TDS Deduction Process

- Determine Applicability: Assess whether TDS applies to the payment being made to the foreign entity.

- Calculate TDS: Compute the TDS amount based on the applicable rate.

- Deduct TDS: Deduct the calculated TDS amount from the payment before remitting the funds.

2. Deposit of TDS

- Timeline: The deducted TDS must be deposited with the government within the stipulated time frame, typically within 7 days from the end of the month in which the deduction is made.

- Challan: Use the appropriate challan (ITNS 281) for depositing TDS.

3. TDS Returns

- Filing Frequency: TDS returns must be filed quarterly using Form 27Q for payments to non-residents.

- Details Required: The return should include details of the deductee, payment amount, TDS deducted, and TDS deposited.

4. Issuance of TDS Certificate

- Form 16A: After filing the TDS return, a TDS certificate (Form 16A) should be issued to the foreign entity, detailing the TDS deducted and deposited.

Common Mistakes to Avoid in Foreign Remittance TDS

When dealing with TDS (Tax Deducted at Source) on foreign remittances, it's crucial to avoid common pitfalls to ensure compliance and avoid penalties. Here are some key mistakes to watch out for:

1. Improper Classification of Payments

Ensure accurate classification of payments (e.g., royalties, fees for technical services) to apply the correct TDS rates.

2. Not Obtaining Tax Residency Certificate

Failing to obtain a Tax Residency Certificate (TRC) from the recipient can lead to higher withholding tax rates.

3. Ignoring Double Taxation Avoidance Agreements (DTAA)

Not considering applicable DTAAs can result in over-taxation. Always check for treaty benefits.

4. Incorrect TDS Rate Application

Using incorrect TDS rates can lead to under-deduction or over-deduction, resulting in penalties.

5. Failure to Deposit TDS on Time

Late deposit of TDS can attract interest and penalties. Ensure timely compliance with deposit deadlines.

6. Not Filing TDS Returns Accurately

Inaccurate TDS return filings can lead to discrepancies and penalties. Double-check all details before submission.

7. Neglecting Documentation

Failing to maintain proper documentation (invoices, agreements) can complicate audits and compliance checks.

8. Ignoring Currency Fluctuations

Not accounting for currency conversion rates can affect TDS calculations and payment amounts.

9. Assuming TDS is Not Applicable

Believing that TDS does not apply to certain foreign remittances can lead to legal issues. Always verify applicability. By avoiding these common mistakes, you can ensure smooth compliance with TDS regulations on foreign remittances.

Double Taxation Avoidance Agreement (DTAA)

Overview of DTAA

India has entered into Double Taxation Avoidance Agreements (DTAAs) with various countries to avoid taxing the same income twice. Under these agreements, residents of the contracting countries can claim relief from double taxation.

TDS Implications under DTAA

- Reduced Rates: DTAAs often provide for reduced TDS rates on specific payments, such as royalties and technical fees.

- Tax Residency: To avail of DTAA benefits, the recipient must provide a Tax Residency Certificate (TRC) issued by their home country’s tax authority.

Claiming Benefits under DTAA

- Obtain TRC: The foreign entity must obtain a TRC from its local tax authority.

- Submit TRC: The TRC should be submitted to the Indian payer to claim reduced TDS rates as per the DTAA.

- Compliance with Local Laws: The foreign entity must comply with the tax laws of its home country to benefit from the DTAA.

Best Practices for Managing TDS on Foreign Remittances

- Understand Applicability: Always assess whether TDS applies to the particular remittance and the nature of payment.

- Stay Updated: Keep abreast of changes in TDS rates and regulations to ensure compliance.

- Maintain Documentation: Maintain records of all transactions, TDS calculations, and certificates issued.

- Consult Professionals: Engage tax professionals like Tripathi & Arora Associates for guidance on complex transactions and compliance.

Consequences of Non-Compliance

Penalties for Non-Compliance

Failure to comply with TDS regulations can lead to severe penalties, including:

- Interest: Interest on the amount of TDS not deposited at the prescribed rate.

- Penalties: Penalties for late filing or non-filing of TDS returns.

- Disallowance of Expenses: The TDS amount not deducted may be disallowed as an expense in the payer’s income computation.

Legal Consequences

Non-compliance can also lead to legal action by tax authorities, including assessments and audits.

Conclusion

Navigating the intricacies of TDS implications for foreign remittances is essential for businesses engaged in international transactions. Understanding applicable TDS rates, compliance requirements, and leveraging DTAAs can help minimize tax liabilities and ensure compliance with Indian tax laws. At Tripathi & Arora Associates, we are committed to providing expert guidance and support to businesses in Delhi NCR and beyond.

Our team of professionals can assist you in managing your TDS obligations effectively, ensuring that you focus on your core business operations while we handle the complexities of taxation. For more information on TDS implications for foreign remittances or to schedule a consultation, contact us today!